Thursday, December 08, 2016

More Democratic Twitter Needed?

Would Hillary have won if she had used Twitter more, in the fashion of Donald Trump? It occurs to me that Michigan football coach Jim Harbaugh is another successful user of Twitter. Twitter allows one to bypress the press corps, the gatekeepers with regard to the news that gets reported and discussed. Could this be a good thing, or is it a necessary evil until we find something better? Probably both of these are correct, and this is just aspect of the larger desire for change.

Tuesday, December 06, 2016

Sensible, Centrist Democrats Realize They've Been Had

Kevin Drum writes today that Republicans Don't Care About Keeping Jobs in America. He writes that Obama tried to create incentives for multi-nationals to keep jobs in the U.S., but were ignored by Republicans.

The larger consideration is that some of us have been trying to get the attention of the Democratic party leaders (Obama and Clinton in particular) to make these points for the last 7-8 years:

UPDATE 12/7/2016: Today Drum posts this:

Income Inequality Doesn't Have to Spiral Out of Control

Will concern for the working class finally outweigh concern for put-upon American multinational corporations? It never did while Obama was president, and there's no special reason to think it will now.He ignores the fact that Trump won the Republican primary on this issue.

The larger consideration is that some of us have been trying to get the attention of the Democratic party leaders (Obama and Clinton in particular) to make these points for the last 7-8 years:

- Dem leaders gave more credence to Republican nonsense than to progressive opinions. While the Republicans were clearly trying to obstruct governance by the Obama Administration, progressives were pleading for more worker friendly policies. Obamacare is basically a Republican plan. Progressive calls for single payer were ignored. Similarly, the Obama Administration strove for a counterproductive grand bargain with Republicans on Social Security, and ended up getting the sequester (fiscal austerity). Progressives arguments were ignored.

- In spite of recognizing and calling attention to the middle class stagnation caused by austerity and Republican obstructionism, Obama and Hillary claimed the economy as their own and took credit for it. Drum spent 2015 saying that the economy was strong, for example.

Now Drum realizes that efforts to keep jobs in the U.S. were thwarted by Republicans.

It does make me wonder, though. Hindsight is 20/20 and all that, but why didn't Hillary Clinton make this stuff into a major campaign issue? It would have helped her against both Bernie Sanders and Donald Trump, but she barely ever mentioned these kinds of reforms. Odd.That's what some of us were wondering before the election. That why I voted for Bernie Sanders and Jill Stein. Why would I vote for people who ignored me for many years in favor of Republicans.

UPDATE 12/7/2016: Today Drum posts this:

Income Inequality Doesn't Have to Spiral Out of Control

Apparently you can run a thriving modern economy that benefits the working class as well as the rich. And note that this is pre-tax income. If social welfare benefits were included, the working class in France would be doing even better compared to the USThis from the guy who argued incessantly during the presidential campaign that the U.S. economy was doing great and therefore we should vote for Clinton over Sanders or Trump.

Wednesday, November 30, 2016

Brooksian Centrism

David Brook's latest column is entitled The Future of the American Center.

Brooks makes a good point in noting the following:

the coming Congress may not look like the recent Congresses, when party-line voting was the rule. A vote on an infrastructure bill may look very different from a vote on health care or education or foreign policy. This may be a Congress with many caucuses — floating coalitions rather than just follow-the-leader obedience.

Meanwhile, as Christopher DeMuth wrote recently in The Wall Street Journal, committee chairmen may reassert authority against the executive branch. Trump’s authoritarian style represents an assault on the traditional separation of powers. He may end up energizing all those constitutional forms and practices he stands against.

What’s about to happen in Washington may be a little like the end of the Cold War — bipolarity gives way to multipolarity. A system dominated by two party-line powers gives way to a system with a lot of different power centers. Instead of just R’s and D’s, there will be a Trump-dominated populist nationalism, a more libertarian Freedom Caucus, a Bernie Sanders/Elizabeth Warren progressive caucus, a Chuck Schumer/Nancy Pelosi Democratic old guard.

I’ve been trying to figure out where we’re headed after this election, and I really don’t know. Trump is unpredictable.

But then Brooks goes off the rails, in my opinion:

The most important caucus formation will be in the ideological center. There’s a lot of room between the alt-right and the alt-left, between Trumpian authoritarianism and Sanders socialism…

suddenly there’s a flurry of activity between the extremes… For example, Bill Kristol and Bill Galston have worked in the White Houses of different parties and had voted for the opposite presidential candidates in every election for four decades. But Donald Trump has reminded them how much they agree on the fundamentals.

The most active centrist organization, No Labels, began six years ago in opposition to polarized, cutthroat politics.

Simon Maloy at Salon wrote what is, in my opinion, a cogent rebuttal -- More bogus “new centrism” from David Brooks. Excerpts from Maloy’s critique:

“We stand together against an alternative right disdainful of the traditions of American conservatism and a vocal left that blends socialist economics with identity politics,” Galston and Kristol wrote, echoing Brooks’ alt-right/”alt-left” dichotomy.

This is completely blinkered, so let’s set a few things straight. The “alternative right” is not defined by its disdain for “the traditions of American conservatism.” It’s a racist, white-nationalist, pseudo-intellectual agglomeration of cranks and bigots who now have a direct line to the Oval Office. Only by denuding it of its core evils can one even begin to draw any sort of comparison between the “alternative right” and the “vocal left,” whose disqualifying sins apparently include pushing for universal health care and advocating on behalf of those marginalized by the political system...

No Labels and the rest of the centrist bleaters will instead celebrate the transparently false promises of a balanced budget that will surely attend all this ideological warfare... Toothless centrism appeals exclusively to “retired establishment types,” financiers and “think-tank johnnies” precisely because it is divorced from practical concerns: When you don’t have to worry about rising health insurance premiums or unaffordable mortgage payments, it’s easier to think of a balanced federal budget as the greatest good that government can aspire to.

- Secure Social Security & Medicare for the next 75 years

Social Security and Medicare are not sustainable on their current trajectories due to the retirement of the enormous Baby Boom generation, falling birth rates, and rising healthcare spending. - Balance the federal budget by 2030

If the money we spend as a nation consistently outpaces the money we bring in, the burden of our increasing debt — including the interest we pay on it — will crush us. Unfortunately, that’s where we’re headed.

In summary, Brooks’ advocacy of centrism seems reasonable enough, and much of it is intelligent and constructive, but he makes two serious errors, in my opinion:

- False equivalency between Trumpian authoritarianism and Sanders socialism.

As a final thought, the Democrats have been played (taken advantage of) by the Republicans on the issue of the national debt for the last 40 years. There is no doubt that the Democrats have been more serious about the debt, and it has cost them politically. Reagan, for example, gave lip service to the debt, but increased it with tax cuts and big military spending. George W. Bush likewise cut taxes while invading and occupying Iraq. Obama was more frugal. Trump seems to be well aware of the advantages of the Reagan approach.

Monday, November 14, 2016

Liberals, Progressives, and Radicals

Here's a thought-provoking article that categorizes the left side of the U.S. electorate as liberals, progressives, and radicals:

Richard Kline: Progressively Losing.

Here's my slant on this:

Richard Kline: Progressively Losing.

Here's my slant on this:

- Liberals are socially liberal while fiscally conservative.

- Progressives see the need for continuous change to keep up with changing technology and its effects.

- Radicals are militants driven by extremely difficult personal or community circumstances.

These are all reasonable positions, although I happen to prefer the progressive to the liberal attitude.

Identity Politics, Special Interests, and the Trump Victory

Democrats rallied around various minority groups, thinking this would guarantee victory as straight, Anglo whites are no longer a majority, but rather a plurality. Add in a strong percentage of the white women's vote, and the road to victory via identity politics was clear.

But to many, including various minorities and women, this identity politics looks like special interest politics. People are self-interested, and voted against the "special interests". Hence, Trump won. In my opinion, people voted in their perceived self-interest as opposed to against minorities. Depicting the largely self-interested and politically apathetic class as racists and/or sexists didn't help to win their votes.

A better approach, in my opinion, is to aim to achieve specific economic goals which will be beneficial to the majority of citizens, regardless of ethnicity, gender, or sexual orientation. Here are a few:

But to many, including various minorities and women, this identity politics looks like special interest politics. People are self-interested, and voted against the "special interests". Hence, Trump won. In my opinion, people voted in their perceived self-interest as opposed to against minorities. Depicting the largely self-interested and politically apathetic class as racists and/or sexists didn't help to win their votes.

A better approach, in my opinion, is to aim to achieve specific economic goals which will be beneficial to the majority of citizens, regardless of ethnicity, gender, or sexual orientation. Here are a few:

- government paid health care

- expanded free education

- job guarantee / "infrastructure" projects (put people to work doing socially useful things)

The right will launch vicious counterattacks against these proposals, but the great majority of citizens would stand to benefit from such programs. The main line of attack will be that we can't afford these programs, and that taxes will have to rise to pay for them. That line of attack is untrue. Republicans have repeatedly shown that "deficits don't matter" (that's what Reagan proved, according to Dick Cheney). Trump just got elected on a platform of blatant disregard for fiscal discipline. He even correctly pointed out at one point that the U.S. government can create money to pay any and all debts. Although he basically gave lip service in other speeches to the evilness of the debt, it was just token acknowledgment of the Republican dogma. Bernie Sanders' approach was similar.

In sum, propose good economic programs that all can benefit from. Be prepared to counter false claims that the programs will require tax increases. The deficit can rise, and voters have shown that they really don't care about the deficit. What they care about, rightly, are taxes, government services, and inflation. If we keep are eye on these facts, we can take back the presidency and pass some progressive laws.

UPDATE: Here's what commenter stefan came up with:

UPDATE: Here's what commenter stefan came up with:

Thursday, November 10, 2016

An Optimistic Take on the Election

I don't like Donald Trump, but he is unlikely to follow up on his surprising triumph with a Reagan like transformation of government. He is extremely unpopular among both Democrats and Republicans. Reagan was a gifted orator and connected well with his audiences. Trump is a clumsy buffoon. He was elected because people are upset with the status quo.

Hillary would have been a deeply unpopular president also. That's perhaps not her fault, but she's just been a target for too long and has too much baggage. In my opinion, the Bernie Sanders' campaign was a real surprise. He might have been able to win the general election, but people weren't ready to abandon what had previously worked with Bill Clinton and Obama. Now that that's over, the path is clear for the Bernie wing to provide a clear alternative moving forward. Let's turn over the party to a new generation and reclaim power, while Trump struggles with the incoherent factions in his own party.

Compared to a more "respectable" Republican, Trump is better with regard to trade and war, in my opinion. His position on immigration reflects popular opinion. He is worse on the environment than most. He is lacking in leadership and administrative prowess, which bodes well for Democrats comeback attempts.

So the Trump election is a bump on the road of progress, as our nation and world struggle to adapt to rapidly changing technological landscape. It's a wake up call progressives need to lead on the important issues.

Compared to a more "respectable" Republican, Trump is better with regard to trade and war, in my opinion. His position on immigration reflects popular opinion. He is worse on the environment than most. He is lacking in leadership and administrative prowess, which bodes well for Democrats comeback attempts.

So the Trump election is a bump on the road of progress, as our nation and world struggle to adapt to rapidly changing technological landscape. It's a wake up call progressives need to lead on the important issues.

Wednesday, November 09, 2016

Election Post Mortem

My opinion, and I could be wrong, is the main mistake the Democrats made was in prematurely taking credit for and defending the status quo. The Republicans are the primary villains, from my perspective, and it was their obstruction that kept the status quo from being more palatable to voters. Instead of calling the Republicans out on this, the Democrats went overboard is claiming that the economy was doing well. Another example of this was "Obamacare", which was a Republican designed program, after all.

I actually thought for a time that Obama would not be reelected in 2012 because of what I just said above. But Mitt Romney was an establishment candidate who didn't get his base enthused. Whereas Romney was emblematic of the financial elite, Trump took the opposite approach by vilifying Hillary's Wall Street ties. For all Trump's faults, he correctly judged the extent of popular discontent with the economy, in my opinion.

An argument can be made that Trump won with racism and xenophobia, but it's not that simple. The Democrats, led by Hillary, played into that dynamic by making "identity politics" a big part of their campaign. It worked for Hillary against Bernie (Bernie Bros were parodied as young naive white men), but backfired in the general election. White men are still opinion leaders in many communities, organizations, and families. Thus, they may have influence out of proportion to their raw numbers.

Here's an example related to the theme of identity politics: Paul Krugman led the charge of Democratic economists in favor of Hillary. Here he is in a June Op-Ed:

I actually thought for a time that Obama would not be reelected in 2012 because of what I just said above. But Mitt Romney was an establishment candidate who didn't get his base enthused. Whereas Romney was emblematic of the financial elite, Trump took the opposite approach by vilifying Hillary's Wall Street ties. For all Trump's faults, he correctly judged the extent of popular discontent with the economy, in my opinion.

An argument can be made that Trump won with racism and xenophobia, but it's not that simple. The Democrats, led by Hillary, played into that dynamic by making "identity politics" a big part of their campaign. It worked for Hillary against Bernie (Bernie Bros were parodied as young naive white men), but backfired in the general election. White men are still opinion leaders in many communities, organizations, and families. Thus, they may have influence out of proportion to their raw numbers.

Here's an example related to the theme of identity politics: Paul Krugman led the charge of Democratic economists in favor of Hillary. Here he is in a June Op-Ed:

This is going to be mostly an election about identity. The Republican nominee represents little more than the rage of white men over a changing nation. And he’ll be facing a woman — yes, gender is another important dimension in this story — who owes her nomination to the very groups his base hates and fears.The question now is whether we double down on identity politics, or try to win based on broadly applicable principles and policies? Of course, I think we should go for the fresh ideas to solve problems. One thing I've noticed is that the old liberal opinion leaders have become rather conservative. For one example, I recall Hillary's stance on "Obamacare", where she was clearly to tired to think of making fundamental changes and said as much. I don't blame her -- going up against the right wing noise machine for years would do that to anyone.

Monday, November 07, 2016

The Socrates Show, with guest Pete Peterson

Socrates: My guest today is Pete Peterson, American businessman, investment banker, philanthropist, and author, who served as United States Secretary of Commerce from February 29, 1972 to February 1, 1973. He is also known as founder and principal funder of The Peter G. Peterson Foundation, which he established in 2008 with a $1 billion endowment. The group focuses on raising public awareness about U.S. fiscal-sustainability issues related to federal deficits, entitlement programs, and tax policies.

Pete Peterson: Thank you Socrates. The national debt is a ticking time bomb. As it says on the front page of our foundation's website, it is mathmatically impossible that we will ever be able to pay back our $20 trillion debt. Taxes will have to skyrocket and government obligations such as Social Security still will not be paid. Our children and grandchildren will be impoverished because we are spending above our means.

Socrates: Balancing the budget is not a reasonable goal, and few countries ever do. As I said, we wouldn't have any government money if the government didn't spend more into the economy each year than it collects in taxes.

Pete Peterson: Supposing for a second that I accept this, then the crucial math regarding future inflation relates the size of an annual government deficit to the size of the economy. Some increase in the money supply each year is appropriate for a growing real economy.

Pete Peterson: Thank you Socrates. The national debt is a ticking time bomb. As it says on the front page of our foundation's website, it is mathmatically impossible that we will ever be able to pay back our $20 trillion debt. Taxes will have to skyrocket and government obligations such as Social Security still will not be paid. Our children and grandchildren will be impoverished because we are spending above our means.

Socrates: Bravo to you for thinking about future generations! Surely you have their best interests at heart. $20 trillion is a huge number, and as you say "it's simple math". I did notice, however, that over $5 trillion of this debt is owed to other U.S. government agencies; i.e. it's money that one part of the U.S. government owes to another. Wouldn't it make more sense to net this out from the total you cite?

Pete Peterson: Even if you do that, the national debt is still an enormous $15 trillion.

Socrates: Fair enough. Of that remaining $15 trillion, approximately $5 trillion is held by the central bank (Federal Reserve). Shouldn't that also be considered money that government owes itself, and therefore netted out?

Pete Peterson: No, of course not. The central bank is not part of the United States government.

Socrates: Well the president does appoint the Board of Governors, and 98% of the Fed's profits are transferred to the U.S. Treasury. It was created by an act of Congress, which spells out its social purpose and regulates its means for achieving that purpose.

Pete Peterson: I'll grant that the Fed would have little incentive to profit from the U.S. government debt it holds, at the expense of its mission to serve the public interest, since those profits just go back to the U.S. government. But still that leaves a massive $10 trillion debt which will bankrupt our grandchildren and retirees of the future.

Socrates: Yes, indeed. As you say, the math is simple. Some people do note that that the $5 trillion of debt held by the Federal Reserve was purchased by creating money out of thin air. Why is the $10 trillion debt a problem if it can be monetized (liquidated) by the Federal Reserve in this manner at any time?

Pete Peterson: Of course that would cause massive inflation and we would be the same as the Weimar Republic and Zimbabwe.

Socrates: But the Fed has already monetized $5 trillion (through routine open market operations as well as the recent quantative easing measures) and we don't yet seem be in a comparable situation.

Pete Peterson: That is indeed something of a puzzle. Well I have to admit that monetization is an option, as that is what we've been doing recently to the tune of $5 trillion. But to run a government based on continual monetization will ultimately lead to debasement of the currency and a Zimbabwe like situation. Everyone knows this.

Socrates: Quite so. Everyone realizes that taxes are necessary, and that there is a limit to the extent of fiscal deficits before severe inflation takes hold. This is where the math kicks in, in trying to determine those limits.

Pete Peterson: Now you are making good sense. I love math (preferably simple)!

Socrates: Here is an equation that I've been contemplating. Sovereign Debt = Money.

Pete Peterson: Ha ha. Everyone knows that money is something you own free and clear, whereas debt is something you owe. Obviously these are totally different.

Socrates: But what about if you are the creditor with regard to the debt? So money is something you own free and clear, whereas the debt you hold is also something you own free and clear. The money is perfectly liquid, whereas the debt you hold is not as liquid, yet pays interest. An analogy is that the money you hold is like an electronic checking account, or demand deposit. Whereas the government debt you hold is like an electronic savings account, or time deposit. They're two different forms of money.

Pete Peterson: You're blowing my mind here. Everyone knows that government debt is bad because we the people, as represented by the government, owe others.

Socrates: Right. But the other side of the government debt is that people or organizations in the private sector are owed that money. Anyone who owns U.S. Treasuries in effect has a time deposit with the U.S. government.

Pete Peterson: Whatever. Don't the Chinese hold most of our Treasuries, anyway?

Socrates: Yes, the Chinese and other foreign entities do own about $5 trillion of our outstanding $10 trillion debt (see here). They buy this debt on the open market. Because the Chinese have a huge trade surplus with the United States, they end up with a lot of cash (demand deposits), and exchange this for Treasury bonds (time deposits), so that they can earn a bit of interest.

Pete Peterson: Just as I thought. We're deeply in debt to the Chinese.

Socrates: A better way to think of that might be to say that the Chinese hold a lot of U.S. dollars because of our massive trade deficit. Whether they hold cash or Treasury bonds is irrelevant. The trade deficit is the issue here, and that is a separate issue from the national debt and fiscal deficit.

Pete Peterson: Hmmm. I guess that makes sense. But I'll have to think about it some more because that doesn't jibe with the usual narrative.

Socrates: Fair enough. I'll wait while you think........

Pete Peterson: Ok. I'm ready to continue. I guess it makes sense that the Chinese will hold a lot of our dollars if they accept dollars for their exports, and have a lot more exports as compared to the dollars they need to spend on imports. This doesn't have anything directly to do with the U.S. fiscal deficit, but rather is because of global trade practices.

Socrates: I'm glad we can agree on some of these issues. You're okay, Pete.

Pete Peterson: You're not so bad yourself, Soc. So, getting back to the debt as opposed to the money supply, I am beginning to see that there are similarities. And that would explain why we didn't get any more inflation when we "monetized the debt". We just exchanged one form of money for another -- demand deposits for time deposits.

Socrates: Yes. You've been listening!

Pete Peterson: But I would have thought that people would spend more when their assets were in demand deposits (cash) as opposed to time deposits (U.S. Treasury bonds). After all, you can't spend bonds directly. The duration of the bonds forces people to save.

Socrates: It turns out that U.S. bonds are the most liquid assets in the world (after cash). You can exchange them for cash any time at a market rate. U.S. Treasury bonds are also the gold standard as collateral for loans. U.S. Treasury bonds serve much the same function as gold did back in the days of the gold standard.

Pete Peterson: No way!

Socrates: At any rate, no one would forego a purchase because they held U.S. bonds instead of cash. It is a trivial matter to exchange your bonds for cash and make the purchase. So that's why there has been no increase in inflation as the Fed has monetized debt.

Pete Peterson: I've got to admit that answers a question that has been puzzling me. So even though we've liquidated $5 trillion of "debt" by exchanging money for U.S. bonds, that hasn't really affected the overall money supply, which includes demand deposits (U.S. currency and checking accounts) and time deposits (U.S. bonds). So the total amount of outstanding "debt" is not really the important figure in the math. You've got to consider the money and the "debt" together.

Socrates: That's right. It's still fairly simple, right? Whether the government finances deficit spending by creating money or interest-bearing bonds doesn't really matter that much. The key is the annual deficit, not the form of IOU (demand deposit or time deposit), spent into the economy.

Pete Peterson: Right. Thanks for reminding me of my main concern. We shouldn't have any annual fiscal deficits.

Socrates: Well, if we didn't have fiscal deficits, we wouldn't have any government money. That's another important part of the math.

Pete Peterson: Whoa! Everybody knows we should balance the budget, yet we never do.

Pete Peterson: Come to think of it, where does money come from in the first place?

Socrates: Now you're getting it. U.S. dollars come from the U.S. government, or its authorized agents, the commercial banks. Commercial banks also create U.S. dollars, but these are offset by obligations to pay back the dollars. We can discuss the banking system later, if you're interested. The bottom line is that the private sector's net money all comes from fiscal deficits.

Pete Peterson: Supposing for a second that I accept this, then the crucial math regarding future inflation relates the size of an annual government deficit to the size of the economy. Some increase in the money supply each year is appropriate for a growing real economy.

Socrates: Exactly right. And speaking of the real economy, that is what we need to consider with regard to the health of future generations. What will matter to my grandchildren is the civil society, infrastructure, and productive capacity they inherit.

Pete Peterson: So by spending less (or taxing more), we could actually be impoverishing the world of our grandchildren, if we neglect our environmental, technological, and human capital?

Socrates: Right again. Do you think it will matter to future generations if the amount of money (cash + bonds) in circulation is $50 trillion or $100 trillion?

Pete Peterson: It shouldn't make a difference. Rather, it is real wealth -- productive capacity, strong civil institutions, a healthy environment, healthy and well educated people -- that will matter.

Socrates: I couldn't have said it better myself.

Pete Peterson: But I worry about the distribution of financial wealth. Aren't we promising too many entitlements to seniors and others who won't be working? As baby boomers retire, this non-productive part of the population will become a larger burden on those who do work.

Socrates: Right. This is a legitimate concern. Personally, I'm in favor of promising a decent living to future retirees at government expense. At best, this will stimulate the economy and provide better job opportunities with higher compensation for future workers as seniors consume relatively more goods and services. At worst, it will cause inflation as workers are unable to keep up with the demand from seniors. My best guess is that the best case is more likely than the worst case, as increasing productivity and technological advances eliminate many of the old jobs.

Pete Peterson: We'll know on that fateful day in 2035 when the Social Security Trust Fund is depleted (according to the most recent forecast).

Socates: Right. My best guess is that we'll do what we currently do with the general government running a deficit, and that is nothing other than continue to pay the bills and occasionally extend the debt ceiling. If inflation becomes a problem, the future can deal with it at that time by lowering the deficit. But there is nothing in the math that guarantees inflation in 2035, anymore than our current deficit guarantees inflation. Demographics are certainly a factor, but so are many more variables including productivity, international trade, sustainable technology, and the state of our human capital.

Pete Peterson: But I worry about the distribution of financial wealth. Aren't we promising too many entitlements to seniors and others who won't be working? As baby boomers retire, this non-productive part of the population will become a larger burden on those who do work.

Socrates: Right. This is a legitimate concern. Personally, I'm in favor of promising a decent living to future retirees at government expense. At best, this will stimulate the economy and provide better job opportunities with higher compensation for future workers as seniors consume relatively more goods and services. At worst, it will cause inflation as workers are unable to keep up with the demand from seniors. My best guess is that the best case is more likely than the worst case, as increasing productivity and technological advances eliminate many of the old jobs.

Pete Peterson: We'll know on that fateful day in 2035 when the Social Security Trust Fund is depleted (according to the most recent forecast).

Socates: Right. My best guess is that we'll do what we currently do with the general government running a deficit, and that is nothing other than continue to pay the bills and occasionally extend the debt ceiling. If inflation becomes a problem, the future can deal with it at that time by lowering the deficit. But there is nothing in the math that guarantees inflation in 2035, anymore than our current deficit guarantees inflation. Demographics are certainly a factor, but so are many more variables including productivity, international trade, sustainable technology, and the state of our human capital.

Pete Peterson: I'll have to ponder this now that I realize that government debt is essentially the same as government money, and that the total is less important than how it is distributed.

Socrates: The ownership society of the last 35 years has resulted in a large change in the distribution of income from workers to owners of capital. You could say that workers have earned their promised social security payments, and that we should look elsewhere if distribution of wealth is our concern.

Pete Peterson: Fair enough. I will feel better knowing that my grandchildren won't have to worry about me, and my foundation's employees, eating cat food when we retire.

Socrates: Right. The math isn't really so simple, I'm afraid.

Pete Peterson: Fair enough. I will feel better knowing that my grandchildren won't have to worry about me, and my foundation's employees, eating cat food when we retire.

Socrates: Right. The math isn't really so simple, I'm afraid.

Pete Peterson: I guess math isn't my strong suit after all. I overstated the actual "national debt" by 100%, incorrectly including the debt that one part of the government owes to another. I would never make such a mistake in valuing my personal net worth. I compounded that error by failing to notice the convertibility between the supposed debt and money. They are interchangeable, and that has been demonstrated in recent years as $5 trillion of the "debt" has been converted to money without appreciable effect upon the economy. I've confused national wealth, which is best expressed in terms of real assets, with financial numbers on a balance sheet. And, finally, I've framed the real distributional issues in such a way that retirees are to be seen as the problem, while ignoring other distributional factors.

Socrates: Your basic mistake is an example of the fallacy of composition.

Pete Peterson: What's that?

Socrates: The fallacy of composition arises when one infers that something is true of the whole from the fact that it is true of some part of the whole. You are assuming that a currency issuing government must balance its budget, just like the constituent families and businesses. At our individual, private sector, levels, we must balance our budgets, or ultimately go bankrupt. At the national level, where we can create money as needed out of nothing, the real effects on society are what we should be considering.

Pete Peterson: Even if I buy that, we still have to worry about being in debt to China, right?

Socrates: Yes, our foreign debt could be a problem, especially if it's denominated in something other than the U.S. dollar. So I agree that we don't want to leave future generations with a society which chronically needs more from the rest of world than we can give back. But that has little to do with our fiscal budget and rather is a function of our trade balance.

Pete Peterson: Can we just leave it there for now?

Socrates: Absolutely, It's been a pleasure talking with you.

Pete Peterson: Likewise. Ciao.

Socrates: Aloha.

Sunday, May 08, 2016

How We Arrived at Trump v Clinton

The recent London mayoral election, in which Zac Goldsmith lost to Sadiq Khan, reminded me of his father, Sir James Goldsmith, who fought against economic globalization in the early 1990s. There's a famous debate between Goldsmith and Bill Clinton's economic advisor Laura Tyson which took place in 1994 on Charley Rose's interview show -- Goldsmith, Tyson, and Rose discuss expanding economic globalization.

As I see it, Goldsmith warned of the problems we faced and Trump versus Hillary Clinton follows from this discussion as night follows day. Tyson presented the neoliberal Clintonian position that free trade is win-win, while Goldsmith warned that it would be win for the rich capitalists taking advantage of lower cost laber, while labor would lose due to third world competition. Twenty-two years labor, Clinton, supported by Nobel prize winning economist Paul Krugman, represents the status quo in the dysfunctional society predicted by Goldsmith.

In site of several asset bubbles and one severe recession, the conventional wisdom today remains much the same as it was. Obama has been working on two new "free trade treaties", the Trans-Pacific Partnership and the Transatlantic Trade and Investment Partnership.

The following graph shows real household income in the United States, a representative measure of economic well-being. The General Agreement on Tariffs and Trade (GATT) was expanded in 1995, becoming the World Trade Organization. Goldsmith warned that this expansion would result in a lose-lose situation for industrialized and less developed economies. Since China joined the WTO in 2001, this measure of income has decreased significantly.

More reading on the subject:

Why Voters Will Stay Angry

A Progressive Logic of Trade

As I see it, Goldsmith warned of the problems we faced and Trump versus Hillary Clinton follows from this discussion as night follows day. Tyson presented the neoliberal Clintonian position that free trade is win-win, while Goldsmith warned that it would be win for the rich capitalists taking advantage of lower cost laber, while labor would lose due to third world competition. Twenty-two years labor, Clinton, supported by Nobel prize winning economist Paul Krugman, represents the status quo in the dysfunctional society predicted by Goldsmith.

In site of several asset bubbles and one severe recession, the conventional wisdom today remains much the same as it was. Obama has been working on two new "free trade treaties", the Trans-Pacific Partnership and the Transatlantic Trade and Investment Partnership.

The following graph shows real household income in the United States, a representative measure of economic well-being. The General Agreement on Tariffs and Trade (GATT) was expanded in 1995, becoming the World Trade Organization. Goldsmith warned that this expansion would result in a lose-lose situation for industrialized and less developed economies. Since China joined the WTO in 2001, this measure of income has decreased significantly.

Why Voters Will Stay Angry

A Progressive Logic of Trade

Tuesday, March 15, 2016

A Litany of Liberal Economic Confusion in the 21st Century

As a liberal, I've been of the opinion that the Republicans / conservatives have been wildly wrong in terms of the economy since the year 2000. Only recently have I come to feel that the Democratic / liberal conventional wisdom has been similarly clueless (although not to the same degree). Here is a timeline of Democratic economic thinking in support of this observation.

Fighting Fiscal Phantoms. As I described here, that was a complete turnaround, without ever acknowledging he was wrong in the first place. With Krugman as our economic guru, no wonder so many liberals are confused.

Early 2000s: Bush Tax Cuts and Wars

Just as Democrats and centrist Republicans in 1980 predicted economic disaster due to Reagan's voodoo economics, the Democratics in the early 2000s were sure that Bush's Tax Cuts and profligate spending would cause a major economic dislocation. As Paul Krugman put it in 2003:There is now a huge structural gap — that is, a gap that won't go away even if the economy recovers — between U.S. spending and revenue. For the time being, borrowing can fill that gap. But eventually there must be either a large tax increase or major cuts in popular programs. If our political system can't bring itself to choose one alternative or the other — and so far the commander in chief refuses even to admit that we have a problem — we will eventually face a nasty financial crisis.

The crisis won't come immediately. For a few years, America will still be able to borrow freely, simply because lenders assume that things will somehow work out.

But at a certain point we'll have a Wile E. Coyote moment. For those not familiar with the Road Runner cartoons, Mr. Coyote had a habit of running off cliffs and taking several steps on thin air before noticing that there was nothing underneath his feet. Only then would he plunge.

What will that plunge look like? It will certainly involve a sharp fall in the dollar and a sharp rise in interest rates. In the worst-case scenario, the government's access to borrowing will be cut off, creating a cash crisis that throws the nation into chaos.

[Paul Krugman, New York Times, 10/14/2003 http://www.pkarchive.org/column/101403.html ]That turned about to be 180° wrong as Krugman himself acknowledged in 2012:

Fighting Fiscal Phantoms. As I described here, that was a complete turnaround, without ever acknowledging he was wrong in the first place. With Krugman as our economic guru, no wonder so many liberals are confused.

2008: Housing Bubble Leads to Financial Crisis

The leading Democrats, including Barack Obama and Hillary Clinton advisors, were clueless going into the great financial meltdown and recession of 2008. Austan Goolsbee, who was to become Chairman of the Council of Economic Advisers under Obama, praised subprime housing loans in 2007: ‘Irresponsible’ Mortgages Have Opened Doors to Many of the Excluded. Notice the scare quotes around the word irresponsible. My neighborhood in Detroit was one of many devastated by extremely high levels of foreclosures and bank-owned, empty housing Of course, the entire country was plunged into recession and saved from worse only by trillion dollar government bailouts to private financial institutions.

2009: Stimulus Package

The fiscal stimulus passed in 2009 over the objection of almost all Republican Congresspersons. The bill was scaled back considerably to get the support of a few Republicans needed to break a filibuster in the Senate. While this was the probably the best that the Democrats could have accomplished given the political landscape (short of the reconciliation tactic later used to pass ObamaCare), the Democratic leadership never made the case for a more adequate response. Consequently, the Democrats were punished politically, suffering massive defeats in both houses of Congress in the 2010 midterm elections, and losing control of many state governments.2013-2015: Recovery?

As Obama's second term wore on, the leading liberal / Democratic economists began to proclaim recovery. However, it soon had to be acknowledged that the "recovery" corresponded to one of the slowest periods of growth since World War II. Moreover, the recovery was skewed to the wealthy, and wage stagnation has been a fact of life for the middle class. Obama appointed Janet Yellen to take over as head of the Federal Reserve, giving Democrats even greater ownership of the economic status quo.

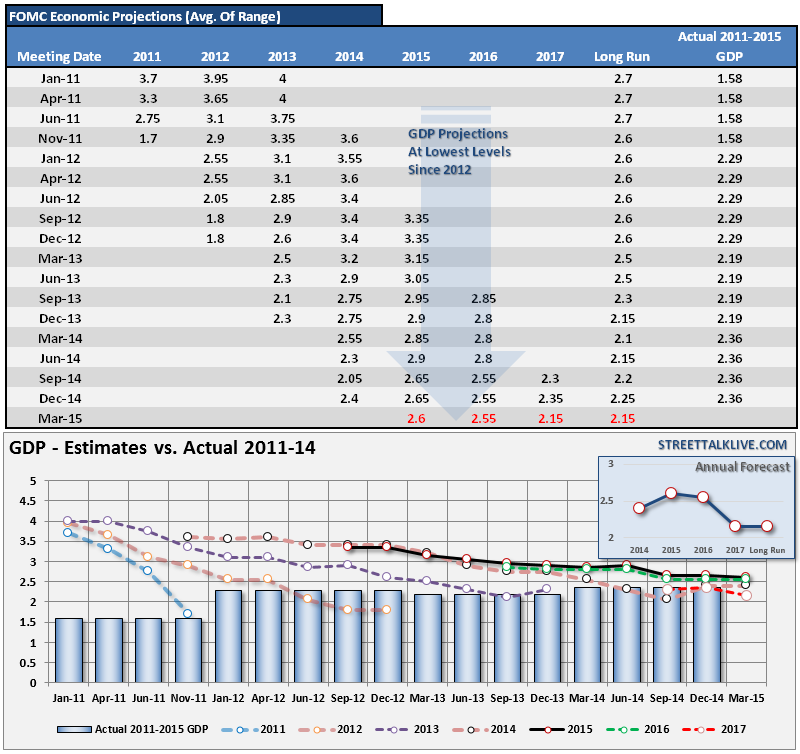

The following chart (source David Stockman) shows how the Fed has consistently overestimated growth:

Thus, for example, the Fed in January 2011 was predicting 4% growth for 2013. The actual growth, as shown in the Dec-13 row was 2.3% (since revised down again to 1.5%). The same pattern occurs for every year in the table.

2015-2016: Reduced Potential

The liberal / Democratic conventional wisdom has now come to grips with the fact that they've been continually over-optimistic. The result has been to lower expectations as to what is possible. This is shown in the diagram above in the "Long Run" column. The long run growth potential of the economy was thought to be an annual rate of 2.7% in 2011 to a rate of 2.15% in 2015.

Kevin Drum in 2012 claimed that 12 million new jobs is the minimum that should be expected over the next presidential term, and that even Romney would have no trouble hitting that. Now that we're on pace for considerably less than that, he seems to be part of the new consensus that we're doing just fine, given our reduced potential.

Liberal Democrat at Bill McBride (at the popular Calculated Risk blog) says that 2% is the new 4%.

This is nonsense, in my opinion. Bernie Sanders' proposals would put a lot more disposable income into the hands of the lower and middle classses, and they would spend it, thus increasing growth. Perhaps we could get annual growth back to the 5%+ of the voodoo-based Reagan era -- bouncing back from a severe recession, as we are now trying to do.

[ John Ross ]

The combination of dramatically slower growth and "ownership society" benefits does not bode well for the younger amongst us.

The Future

U.S. economic growth has slowed dramatically over the last 50 years:[ John Ross ]

The combination of dramatically slower growth and "ownership society" benefits does not bode well for the younger amongst us.

Thursday, March 10, 2016

Untrustworthy Hillary

Hillary's bogus criticisms of Sanders undermine her credibility. A few examples:

There is a fundamental dishonesty at the heart of Hillary's campaign. She is a centrist Democrat in the mold of Bill Clinton and Barack Obama, pretending to be anti-Wall Street. She is in favor of working with sympathetic elements on Wall Street and in the business community. Clinton and Obama have had some successes with this approach. The Clinton and Sanders administrations have relied on Wall Street from Robert Rubin, Clinton's Secretary of the Treasury and former Goldman Sachs and Citigroup chair, to Jack Lew, the current Secretary of the Treasury, and former COO at Citigroup. This is a legacy she could honestly run on, but she's attempting the opposite.

In my opinion, the financial deregulation that Robert Rubin engineered in the late 1990s was a really, really bad idea. This fact is more or less universally acknowledged, but not something that the Clinton team has come to terms with. Bernie's campaign is pressing this issue in a similar manner to the way the Trump campaign is pressing the folly of the Iraq War in Republican discourse.

For Hillary to run an honest campaign, she would have to promote her ties to Wall Street as an advantage, something the electorate does not agree with. Or else, she would have to repudiate much of her legacy with the Clinton and Obama adminstrations which would undermine her Democratic base of support. She's in a no-win situation.

Kevin Drum makes the point that Hillary has been subject to decades of abuse, and, perhaps as a result, is not very direct in communicating her stance on the issues. But there are good reasons that straightforward communications do not come easily at this point in her career.

- She claims that she supported the auto industry and Bernie didn't. In fact, she was referring to TARP (a Wall Street bailout).

- She claims that the Koch brothers support Sanders.

These claims don't pass the smell test. I support Sanders because I like his policy proposals. Hillary also impressed me by seeming to embrace similar proposals. but the longer this campaign goes on, the more I am noticing that she is, in fact, trying to trick us. She is out of touch with reality if she thinks she can credibly outflank Bernie from the left.

There is a fundamental dishonesty at the heart of Hillary's campaign. She is a centrist Democrat in the mold of Bill Clinton and Barack Obama, pretending to be anti-Wall Street. She is in favor of working with sympathetic elements on Wall Street and in the business community. Clinton and Obama have had some successes with this approach. The Clinton and Sanders administrations have relied on Wall Street from Robert Rubin, Clinton's Secretary of the Treasury and former Goldman Sachs and Citigroup chair, to Jack Lew, the current Secretary of the Treasury, and former COO at Citigroup. This is a legacy she could honestly run on, but she's attempting the opposite.

In my opinion, the financial deregulation that Robert Rubin engineered in the late 1990s was a really, really bad idea. This fact is more or less universally acknowledged, but not something that the Clinton team has come to terms with. Bernie's campaign is pressing this issue in a similar manner to the way the Trump campaign is pressing the folly of the Iraq War in Republican discourse.

For Hillary to run an honest campaign, she would have to promote her ties to Wall Street as an advantage, something the electorate does not agree with. Or else, she would have to repudiate much of her legacy with the Clinton and Obama adminstrations which would undermine her Democratic base of support. She's in a no-win situation.

Kevin Drum makes the point that Hillary has been subject to decades of abuse, and, perhaps as a result, is not very direct in communicating her stance on the issues. But there are good reasons that straightforward communications do not come easily at this point in her career.

Saturday, February 27, 2016

Bernie Sanders for the Economy, Part 2

Bernie Sanders for the Economy, Part 2

With regard to Democratic establishment economists who continue to say that Sanders' plans are unrealistic, I have three arguments in favor of Sanders:

- The Democratic economists have a poor track record in making economic predictions.

- Most of Sanders proposals have been succcessfully implemented in developed nations around the world.

- Young people have good reason to support Sanders' economic proposals.

Democratic economists have a poor track record in making economic predictions.

- Democrats in 1980 criticized Reaganomics as unrealistic because of "supply side economics" and consequent budget deficits. Budget deficits have not been a problem since. The real problem with Reaganomics was increasing income inequality, something the Democratic economic establishment missed at the time and continues to underplay.

- Paul Krugman became the foremost spokesman for Democratic economists, yet has been wildly off the mark with regard to the issue of government deficits. See Paul Krugman in 2003 predicts the exact opposite of what has taken place seen then. Krugman has since changed his position 180 degrees with regard to the dangers of too much government spending, but remains attached to the discredited theories which got him to the wrong position in the first place.

- Austan Goolsbe in 2007 praised subprime housing loans, just as the subprime housing loan crisis was evolving into the deepest recession since the 1930s.

- Mainstream economic forecasting around the world has been consistently overoptimistic about economic growth. Inflation has consistently come in below expectations. Yet Democratic economists continue to give the underlying economic models credibility.

- Models favored by the Romers

- Federal Reserve GDP predictions

- Japanese central bank predictions

- European central bank predictions

- OECD predictions

- World Bank predictions

- Council of Economic Adviser predictions

- When forecasts have proven wrong, Democratic economists have responded by lowering estimates of what is potentially achievable. As the Romers say,

Even very generous estimates of the amount of slack still present in the American economy would not be enough to accommodate demand-driven growth of anything near what Friedman is estimating. As a result, inflation would soar and monetary policy would swing strongly to counteract them.

Friedman predicts growth similar to that achieved during the Reagan Administration, and the Romers say this is impossible.

Most of Sanders proposals have been succcessfully implemented in developed nations around the world.

Health Care Financing: It's widely known that every developed country has government mandated universal health care, with comparable or better results than the U.S., and at a fraction of the cost and administrative complexity.

Minimum Wage: Sanders minimum wage proposal ($15/hour) is less than the actual minimum in other developed countries such as Australia.

Higher Education: College is much more heavily subsidized in other developed countries, and much more affordable. For example, college is free in Germany.

Young people have good reason to support Sanders' economic proposals.

Middle class is much less affordable than it used to be. Pensions are no longer guaranteed, health care involves much higher out-of-pocket payments, education is more expensive. Overall, the trend is to get people in debt when they are young, and to let them spend their lives in that state. We can do better than this, and have in the not too distant past, and most other countries do better today.Saturday, February 20, 2016

Bernie Sanders for the Economy

Status Quo Panic

As a supporter of Bernie Sanders, I was upset to hear, a few days ago, of a flurry of panicky articles by elite Democratic economists criticizing Bernie Sanders' ecconomic plans:- An Open Letter from Past CEA Chairs to Senator Sanders and Professor Gerald Friedman

- Worried Wonks, by Paul Krugman

- Bernie Sanders' Campaign Has Crossed Into Neverland, by Kevin Drum

I am overjoyed to see that one of my favorite economists, Jamie Galbraith, has already responded with an open response to the CEA Chairs. And Galbraith's response is typically brilliant, with wit and wisdom.

Furthermore, I found that Kevin Drum has already recanted:

A severely critical letter from former CEA chairs ... roasted Friedman's study without doing any actual analysis of his forecasts... And it turns out that...Friedman isn't projecting anything wildly out of the ordinary after all... I set out to take another whack at these projections, and I didn't really get what I expected. [On Second Thought, Maybe Bernie Sanders' Growth Claims Aren't As Crazy As I Thought]Kudos to Drum for following up and correcting the record. Don't expect any such admission of premature judgment by Krugman, who is notorious for never acknowledging when he is wrong.

As for the substance of the Sanders economic debate, I'll just quote Galbraith:

So, let's first ask whether an economic growth rate, as projected, of 5.3 percent per year is, as you claim, “grandiose.” There are not many ambitious experiments in economic policy with which to compare it, so let's go back to the Reagan years. What was the actual average real growth rate in 1983, 1984, and 1985, following the enactment of the Reagan tax cuts in 1981? Just under 5.4 percent. That's a point of history, like it or not...

When you dare to do big things, big results should be expected. The Sanders program is big, and when you run it through a standard model, you get a big result...

Paul (Krugman) relies on you (the former CEA chairs) to impugn an economist with far less reach, whose work is far more careful, in point of fact, than your casual dismissal of it. He and you also imply that Professor Friedman did his work for an unprofessional motive. But let me point out, in case you missed it, that Professor Friedman is a political supporter of Secretary Clinton. His motives are, on the face of it, not political.

Unfortunately, this episode fits a pattern of panicky status quo reaction to the Sanders phenomenon. In addition, there have been Clinton attacks on Sanders for having temerity to criticize Obama at times over the past 8 years, and on caucus eve, Clinton’s allies warn Nevada Latinos to beware of Bernie Sanders.

Larger Significance

I strongly believe, with regard to the economy, that the Democratic status quo is better than the Republican alternative. But the Democratic status quo is badly flawed, and it doesn't help the team to pretend otherwise. Sanders' proposals are realistic in my opinion, and this becomes clearer the more one examines attacks such as the one described here.

Thursday, February 11, 2016

{kind=link}

{kind=link}

Tuesday, February 02, 2016

One Plausible Scenario in which Trump Wins

I expect Trump to win the Republican nomination (he's got a HUGE lead), but until this morning had not seriously considered the possibility that he might win the presidency. After all, polling shows him to be pretty much unelectable:

Where the book I'm reading (Railroading Economics) comes into play is in its description of the Great Depression. I see a lot of similarities between the economy in the 1920's and that of the current U.S. / global economy. Here are a few:

Railroading Economics explains that the welfare capitalism of the 1920s was an outgrowth of the successful combination of government and business in World War I, and that fascism had a somewhat similar perspective:

I'm a big fan of Bernie Sanders and his brand of democratic socialism. On the other hand, Trump is just the current incarnation of a strong fascist undercurrent running through the electorate. The good news is that Sanders and his socialist platform are far more popular among today's youth. We older Democrats would be wise to consider momentum for change. As John Cassidy notes today in the New Yorker with reference to Bernie Sanders' overwhelming success amongst the younger voters in Iowa:

We’ve got an unpopular set of presidential candidates this year– Bernie Sanders is the only candidate in either party with a net-positive favorability rating — but Trump is the most unpopular of all. His favorability rating is 33 percent, as compared with an unfavorable rating of 58 percent, for a net rating of -25 percentage points. By comparison Hillary Clinton, whose favorability ratings are notoriously poor, has a 42 percent favorable rating against a 50 percent unfavorable rating, for a net of -8 points. [fivethirtyeight.com]While the book I am currently reading may be affecting my judgment, it occurs to me that Trump's favorability, as an extreme outsider, could rise dramatically if the U.S. economy slump dramatically. Suppose, for example, that Hillary wins the Dem nomination and then the economy crashes in the summer or fall, as it did before the 2008 election. In that case Trump the extreme outsider looks much better against Hillary the veteran insider.

Where the book I'm reading (Railroading Economics) comes into play is in its description of the Great Depression. I see a lot of similarities between the economy in the 1920's and that of the current U.S. / global economy. Here are a few:

- Increasing wealth inequality leading to more investment and less consumption (as a proportion of total income)

- Overinvestment leading to decreased returns on productive investment and increasing amounts of questionable financial investment.

- stock markets in bubble territory -- now at 89th percentile, comparable to 1929, 2000, and 2007, and propped up by loans financing stock buybacks.

- junk bonds of questionable value

- An establishment that considers a depression pretty much impossible, and tries to maintain prosperity with the power of positive thinking as opposed to realistic action.

As was the case in 2008 when the U.S. / world plunged into the Great Recession, the overwhelming majority of economists, business, and political leaders view a recession in 2016 as a remote possibility. I have been putting my money against every mainstream economist and beating them all in recent years. Please see:

The latest I've seen is that less than 5% of economists see a greater than 50% chance of recession over the next year. [Financial Times survey of 51 economists]

In the late 1920s and early 1930s, there was a similar sanguinity regarding the possibility of the economy falling into depression. The 1920s was an era of welfare capitalism, and the conventional wisdom was that a depression would not happen because corporate America wouldn't let it. This is what I learned from reading Railroading Economics (linked above),

Hoover believed that the provision of adequate information would suffice for enlightened business leaders to ward off business cycles. (page 165)

The Hoover administration became apostles of the...doctrine that high wages are a guarantee and an essential of prosperity. At the beginning of the depression, Hoover pledged industry not to cut wages, and for a long time large-scale industry adhered to this pledge.In today's economy, employers have been reluctant to lay off employees, despite the sluggish economy, shrinking profits, and soaring inventory levels (although this is not due to presidential jawboning).

During the Depression...the major welfare capitalists quickly realized that the collapse was overwhelming their ability to maintain their commitment to their expressed ideals...The welfare capitalists saw the momentum of the Depression build up. In the face of these pressures, their attempts at carrying out the supposed mandate of welfare capitalism vanished. By the fall of 1931 major corporate employers could no longer refrain from aggressively cutting wages. When push came to shove, unrelenting market forces compelled major firms to renounce all pretenses to the ideals of welfare capitalism. [page 160]

Ultimately welfare capitalism was doomed to failure from the very beginning. Business was incapable of overcoming the tendency of markets to careen out of control. Once the Great Depression struck, people realized that the rhetoric of welfare capitalism was hollow. Most people understood that they could not count on business to protect them from harsh market forces--a lesson that has continued to fade over the subsequent decades. [page 168]Every morning when I watch Bloomberg TV, I am bombarded by optimistic businesspersons and commentators. Mainstream Republicans and Democrats alike are certain that the economy is doing just fine. As noted elsewhere in this blog, I believe the facts point otherwise. And apparently, I am not alone. Just as in the early 1930s, fascist and socialist politicians are popular as people crave an alternative to the status quo.

Railroading Economics explains that the welfare capitalism of the 1920s was an outgrowth of the successful combination of government and business in World War I, and that fascism had a somewhat similar perspective:

Welfare capitalism had the capacity to transform itself into fascism without too much difficulty. It already contained a heavy measure of nationalism and racism. It was more than willing to cede more power to the state, provided that the state would act in the interest of the welfare capitalists. [page 164]The similarities to the Republican party of recent years and the Trump phenomenon are clear. If the economy does slip dramatically this year, then the prospects for the fascists and socialists will be dramatically improved.

I'm a big fan of Bernie Sanders and his brand of democratic socialism. On the other hand, Trump is just the current incarnation of a strong fascist undercurrent running through the electorate. The good news is that Sanders and his socialist platform are far more popular among today's youth. We older Democrats would be wise to consider momentum for change. As John Cassidy notes today in the New Yorker with reference to Bernie Sanders' overwhelming success amongst the younger voters in Iowa:

It is often easier to inspire people, particularly young people, with an uplifting theme than with a resumé. This, of course, was also the problem that Clinton faced in 2008, when Obama ran on a message of hope and the slogan “Yes, we can.” In recent weeks, the Clinton campaign’s response to the Sanders and his promises of ambitious policy actions has sometimes seemed to be “No, we can’t.” In Iowa, at least, that didn’t prove to be a winning message.I don't actually think that this is fair to Clinton. But I see Sanders' policy proposals as the more realistic response to the current precarious economic and political situation. Clinton is offering more of the same, which is certainly better than a descent into fascism, but possibly insufficient to prevent that from happening. If we avoid depression, Sanders will beat Trump handily given Trumps' limited support at present. This is my opinion and receives support from polls such as the one referenced at the beginning of this post. If the economy collapses, Sanders is our best bet to defeat the fascists as he presents a realistic and hopeful alternative to the status quo.

Subscribe to:

Posts (Atom)